By Annmira Joseph

If you have lost your job or experienced a loss in income due to the COVID-19 pandemic, you might want to consider applying for the EPF i-Sinar programme to support your finances. Here’s a quick guide to help you better understand the i-Sinar facility.

Many Malaysians have experienced job losses, salary cuts and forced unpaid leave since the implementation of the first Movement Control Order (MCO) last year. If you’re one of those who were affected and are in need of extra cash to pay off the debts and bills, the Employees Provident Fund (EPF) i-Sinar programme can help you with that.

What is the EPF i-Sinar facility?

EPF i-Sinar or i-Sinar KWSP was announced as a part of the government scheme to support Malaysians who were financially hit by the pandemic, allowing eligible members to withdraw a set amount of funds from their respective accounts.

The EPF has allocated RM70 billion for the initiative, which is expected to benefit eight million members who can withdraw a maximum of RM10,000 or RM60,000, depending on their Account 1 balance. The i-Sinar facility is an extension of the i-Lestari programme which allows a monthly withdrawal of up to RM500 from Account 2, but is scheduled to end this March.

What’s the difference between i-Lestari and i-Sinar?

The i-Lestari is a withdrawal facility that is intended to help members meet their monthly financial needs during the COVID-19 pandemic period. It allows members to withdraw up to RM500 from Account 2 for a maximum 12-month period. This programme runs from April 1, 2020 until March 31, 2021.

i-Sinar, on the other hand, works as an advance facility on your retirement funds. The scheme allows you to withdraw a larger amount of up to RM10,000 (depending on your Account 1 balance), which can benefit those who need large funds upfront. Eligible members will receive an interim payment of up to RM1,000 from the total amount applied on January 26, 2021.

Do you have to replace the i-Sinar withdrawal amount?

Yes, members who choose to apply for i-Sinar are required to channel 100% future EPF contributions into Account 1 until the amount withdrawn is replenished. After that, the contributions will return to the status quo: 70% and 30% to Account 1 and Account 2 respectively.

Who is eligible for i-Sinar?

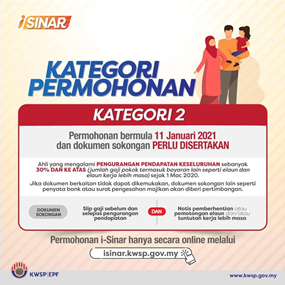

i-Sinar facility is divided into two categories which are Category 1 and Category 2. Below are the details for each category:

Category 1

- Members who have not contributed to the EPF for at least two consecutive months

- Housewives

- Members who are self-employed and work in the gig economy sector

- Members who have lost their jobs

- Members who were given unpaid leave

- Members who have lost their source of income

- Members who are still working but their base salary has been cut by 30% or more since March 2020

- No supporting documents required as the approval will be verified based on EPF data

- Application began on December 21, 2020

- Disbursement started mid-January 2021

Category 2

- Members who are still working and have experienced a reduction in overall income of 30% and above, including salary, allowances and overtime pay since March 2020

- Supporting documents required:

- Salary slips before and after the income reduction, and

- A notice from employer, which states that allowances/overtime claims have been suspended or reduced

- Application begins January 11, 2021

- Disbursement starts the following month after approval

How much can you withdraw from EPF i-Sinar?

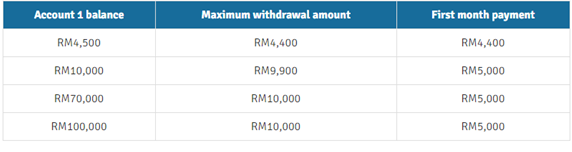

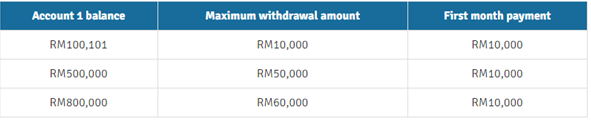

The actual amount that you can withdraw under the i-Sinar facility depends on whether you have more or below than RM100,000 savings in your Account 1. You can choose how much to withdraw in the first payout, but the subsequent payments must be at least RM1,000 per month.

- Account 1 savings ≤ RM100,000

You can withdraw up to RM10,000 while maintaining a balance of RM100 balance in Account 1, The payments will be staggered across six months and you can receive up to RM5,000 for the first payout.

- Account 1 savings > RM100,000

If you are in this category, you can withdraw up to 10% of your savings or up to RM60,000 – whichever is lower. The payments will be staggered across six months, and you could receive a maximum of RM10,000 for your first payout.

How to apply for i-Sinar?

How to check your i-Sinar application status online?

You can check your application status via i-Sinar official website on the “Semak Status Permohonan” (Check Application Status) webpage. Just key in your IC number and mobile number, then click “Semak Status” (Check Status).

If your application has not been approved, the following page will show “Permohonan Anda Sedang Diproses” (Your application is still in process).

Understand your financial situation before applying for i-Sinar

The i-Sinar facility can be useful for those who have lost their jobs, suffered from pay cuts and do not have sufficient funds to sustain their financial lives. Keep in mind that EPF is a scheme that provides monetary benefits to salaried employees after retirement. Therefore, the savings are initially meant to be withdrawn when members have reached the age of 55.

You should only utilise the savings for urgent basic needs. Before applying, check your current financial needs and try to look for other alternatives (if there’s any). Having a proper retirement strategy is a crucial step in helping you live a less stressful future in your older days.

If you need some help in making a decision, we suggest you check out this piece we did on the pros and cons of withdrawing your EPF money under the i-Sinar facility.

Leave a comment